Japan Real Estate Bubble in 1990: What Caused the Crash and Could It Happen Again?

Published On: July 18, 2026

Learn what caused the Japan real estate bubble in 1990, why property prices surged and crashed, and whether a similar housing bubble could happen again.

Table of Contents

Supervised By: Hiroki Kazato

“Has Japan ever experienced a real estate bubble?”

“What was the real estate crash like and how did the land prices drop?”

Japan explained one of the largest real estate bubbles in modern history.

Land prices in Tokyo and other major cities surged throughout the 1980s before collapsing in the early 1990s.

In this article, we explain what happened then and also try to answer the question that many people might have:

Could a similar bubble form in Japan's property market today?

Please read through the article so you can get a deeper understanding of the real estate crisis and the Japanese property market history.

- What Was the Japan Real Estate Bubble in 1990?

- Why Did Property Prices Rise So Quickly?

- How Big Did the Bubble Become?

- What Happened After the Crash?

- Is Japan in a Real Estate Bubble Today?

- Could Another Japan Property Bubble Happen?

- What Can Investors Learn from the 1990 Bubble?

- FAQ

- Summary

1. What Was the Japan Real Estate Bubble in 1990?

The Japan real estate bubble is said to have been triggered by the “Plaza Accord”.

The Plaza Accord was an agreement among the G5 nations to take coordinated action to address the overvaluation of the US dollar.

The aim of the Plaza Accord was to improve US export competitiveness through a weaker dollar and thereby reduce the US trade deficit.

It is called the Plaza Accord because the meeting was held at the Plaza Hotel in New York on 22 September 1985.

The meeting was attended by the finance ministers (including the US Secretary of the Treasury) and central bank governors of the five major industrialized economies—Japan, the United States, the United Kingdom, West Germany, and France (the G5)—at the invitation of the United States.

Specifically, the participating countries agreed to cooperate in bringing about an orderly depreciation of the US dollar against the major currencies through coordinated intervention in the foreign exchange markets.

Meanwhile, in Japan, the rapid appreciation of the yen following the correction of the overvalued dollar contributed to economic stagnation by reducing export competitiveness.

To counter the economic slowdown, the Bank of Japan began a series of policy rate cuts in 1986.

In February 1987, at a G7 meeting, the participating countries concluded the Louvre Accord in Paris to prevent the US dollar from depreciating excessively.

Although exchange rates generally stabilized following the Louvre Accord, the Bank of Japan maintained its low-interest-rate policy because of concerns about a "yen-appreciation recession."

As Japanese companies began to benefit from the stronger yen through lower import costs and overseas investments, the domestic economy gradually recovered.

However, the prolonged period of low interest rates, combined with aggressive lending by financial institutions, created excess liquidity in the economy.

This fueled rapid increases in asset prices, particularly real estate and stocks, leading to the formation of Japan's asset price bubble, commonly known as the "bubble economy."

2. Why Did Property Prices Rise So Quickly?

There were mainly three reasons:

- Land was viewed as a safe investment.

- Businesses and individuals had easy access to credit.

- Property speculation became widespread.

First, there was a widespread belief that Japanese land prices could never fall significantly.

Banks believed that loans would be recoverable as long as land was used as collateral.

In addition, the low-interest-rate policy of the Bank of Japan made borrowing and lending relatively easy.

Competition among banks intensified as they sought to expand their businesses and attract new borrowers.

As a result, excess liquidity flowed into the real estate market.

Supported by easy access to credit, speculation became widespread.

Investors purchased property in anticipation of further price increases, while corporations accumulated real estate assets as investments.

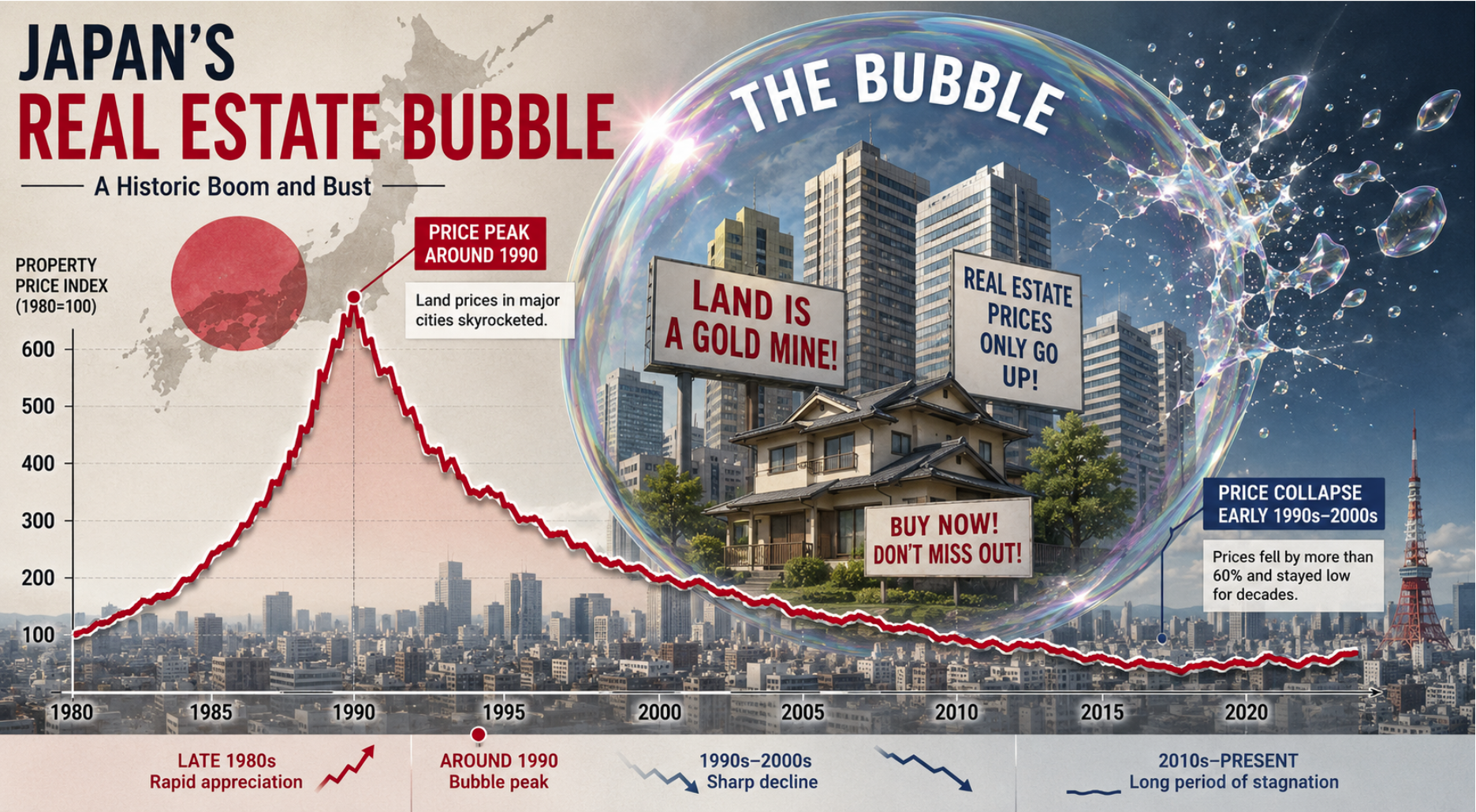

3. How Big Did the Bubble Become?

To understand the sheer scale of the 1990s bubble, we have to look at the staggering speed of price growth.

What started as a steady economic recovery quickly mutated into an unprecedented asset distortion.

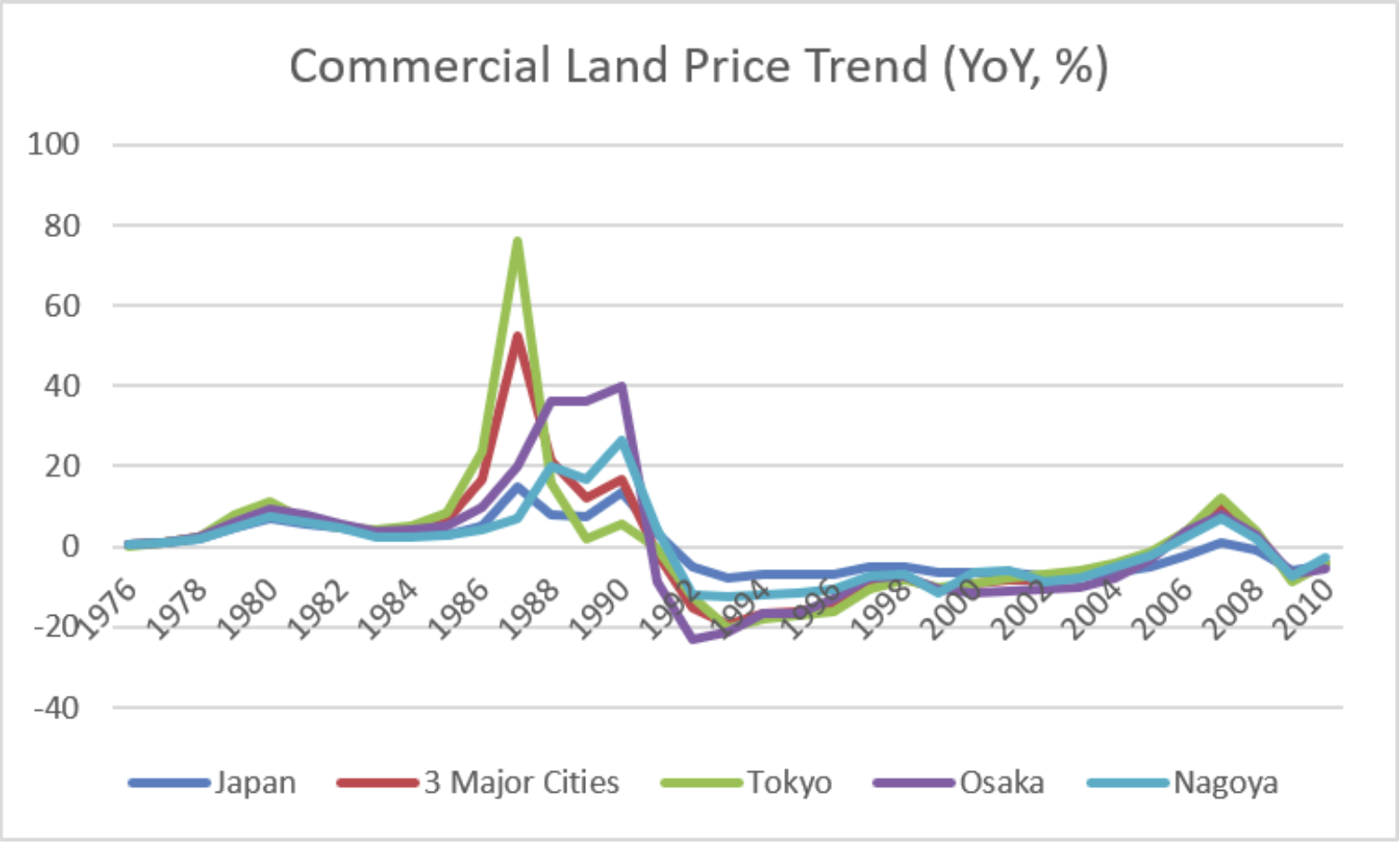

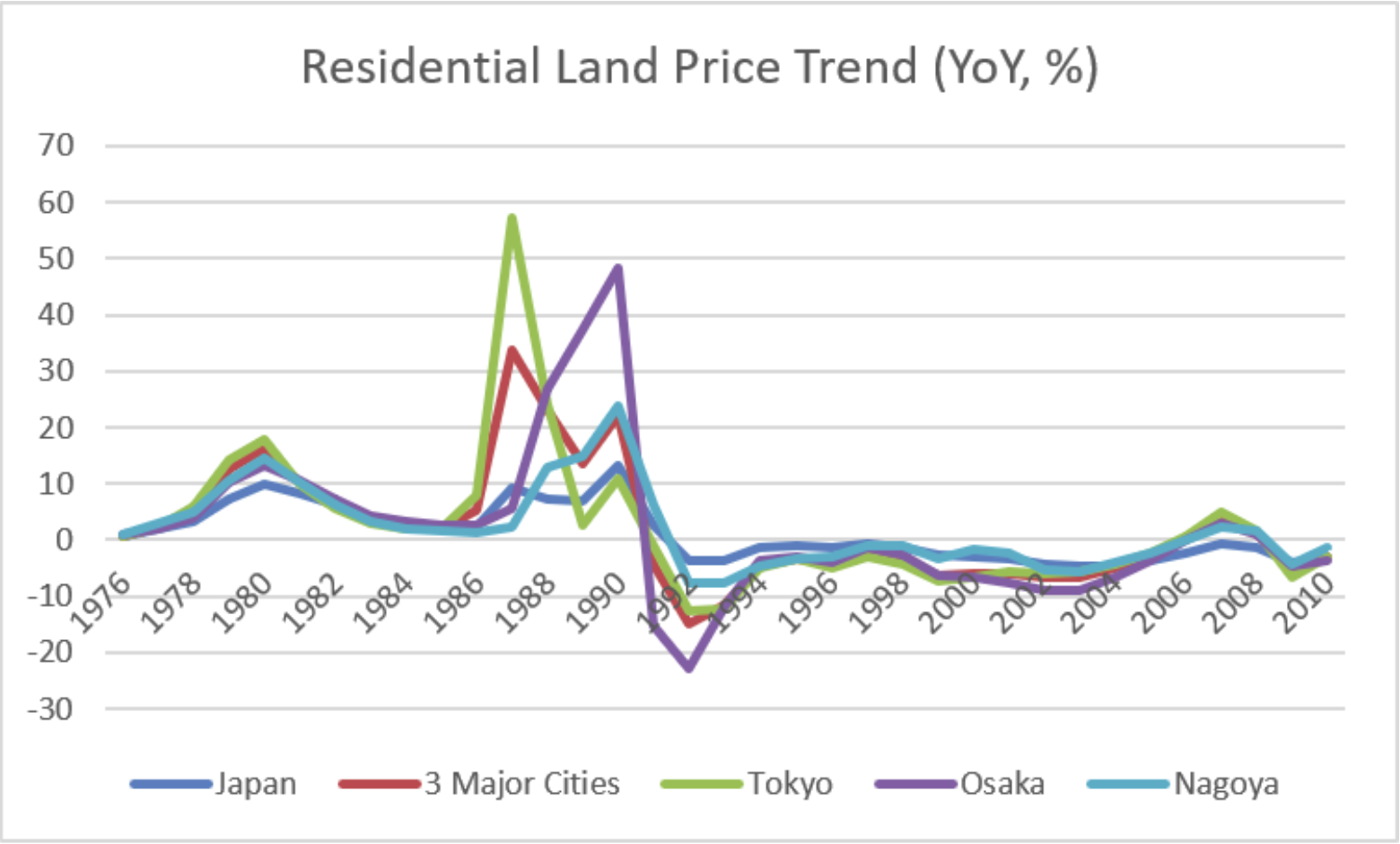

Commercial and Residential Land Growth

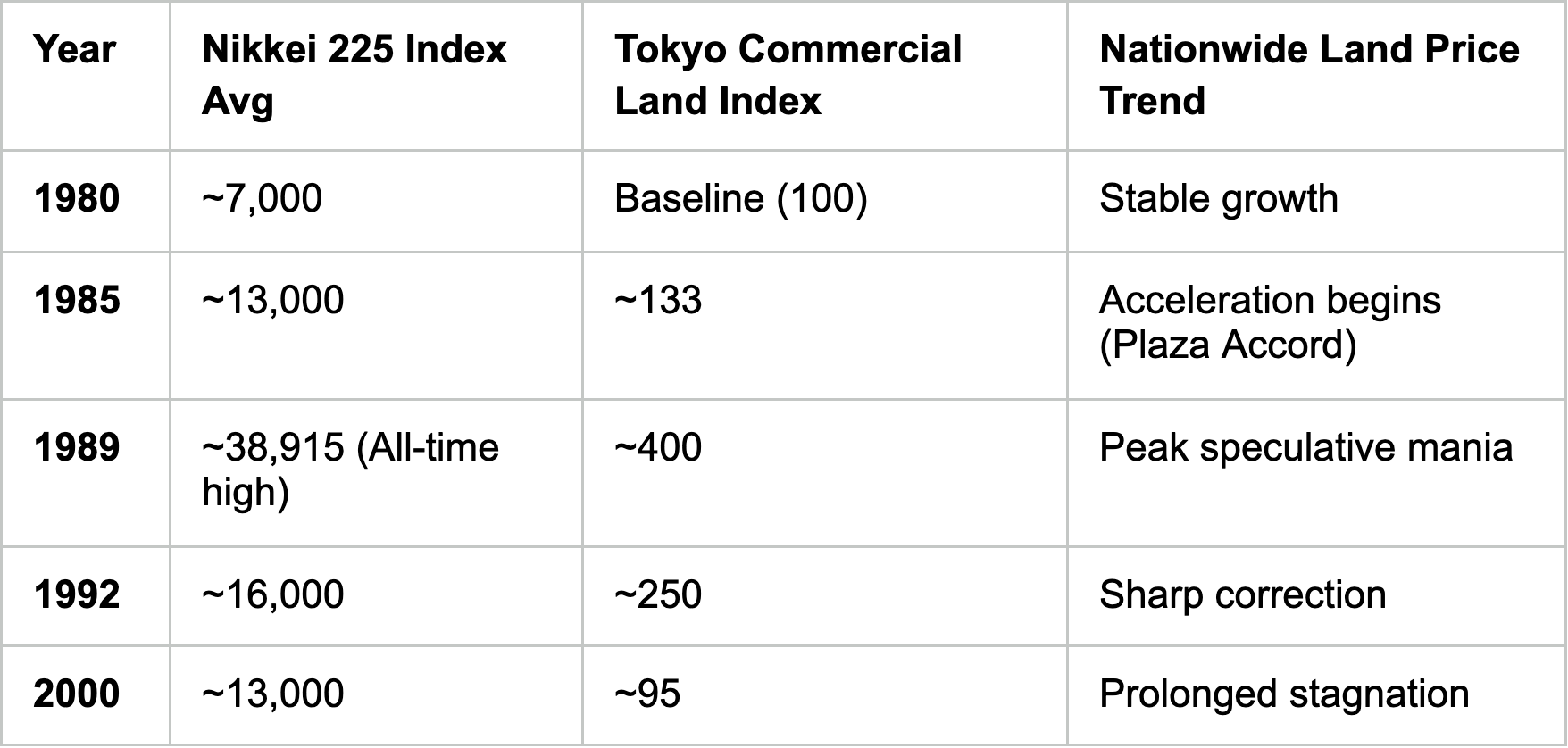

Between 1985 and 1990, commercial land prices in Japan's major cities skyrocketed by over 300%.

Residential zones were not far behind, often doubling or tripling in value in a matter of months.

Neighborhoods that were traditionally working-class suddenly featured homes priced completely out of reach for local families.

Tokyo's Extraordinary Valuations

Tokyo sat at the absolute epicenter of this hyper-inflation.

At the peak of the market in 1989, the total value of all real estate in Japan was estimated to be roughly four times the value of all real estate in the entire United States.

The grounds of the Tokyo Imperial Palace alone were famously calculated to be worth more than the entire state of California or all of Canada.

To visualize this extreme trajectory and its subsequent collapse, consider the general market trend below:

Nikkei 225 Trend Chart (1980 to Date)

Bubbles inherently require a continuous injection of fresh capital to survive.

When the regulatory valves were finally turned to choke off this liquidity, the entire apparatus collapsed with astonishing speed.

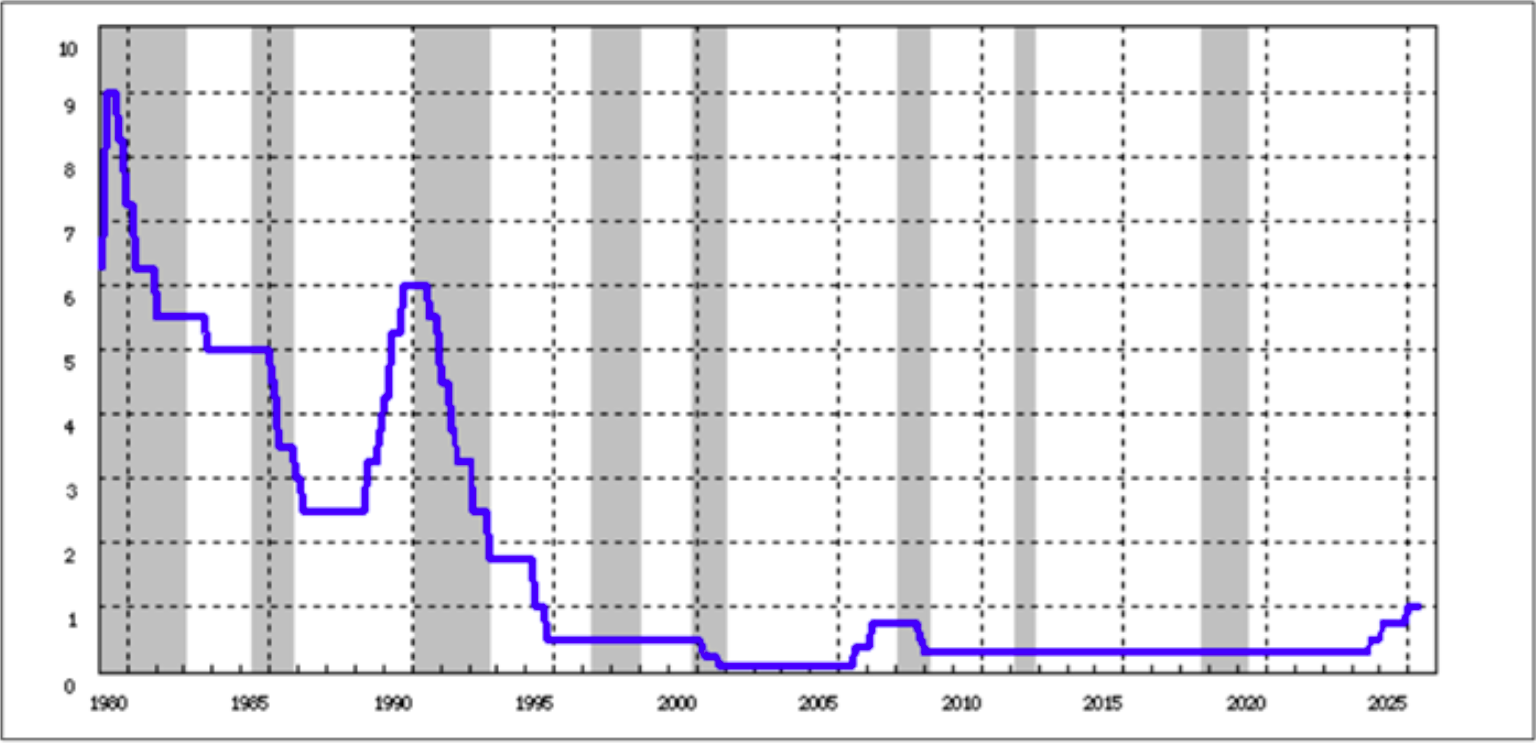

Interest Rate Hikes

Realizing the economy was dangerously overheated, the Bank of Japan radically shifted its monetary policy.

Under the leadership of Governor Yasushi Mieno, the central bank aggressively raised the official discount rate.

It went from a low of 2.5% in 1989 up to 6.0% by August 1990.

This sudden tightening severely increased the cost of carrying massive, speculative debts.

Basic Loan Rate Historical Chart

Lending Restrictions

In tandem with interest rate hikes, the Ministry of Finance introduced a strict regulatory ceiling for real estate loans in April 1990 known as "total volume control" (so-ryo-kisei).

This policy legally restricted commercial banks from expanding their real estate loan portfolios faster than their overall lending growth.

Virtually overnight, the easy-credit spigot that fueled the bubble was turned off.

Falling Investor Confidence

Once the flow of cheap money ceased, property prices stopped climbing.

This static environment proved fatal for speculators who relied entirely on rapid capital appreciation to service their high-interest loans.

- Speculation Reversed: Panicked investors rushed to liquidate assets before prices fell further.

- Forced Sales Increased: Banks began calling in non-performing loans, forcing properties onto an illiquid market.

- Sharp Declines: With an abundance of sellers and no buyers, property values plummeted, erasing trillions of yens in paper wealth.

4. What Happened After the Japan Real Estate Bubble Crash?

The aftermath of the 1990 crash fundamentally altered Japan's economic trajectory, ushering in a painful period of economic stagnation known as the "Lost Decades."

The Lost Decades

The destruction of asset wealth triggered a severe multi-decade economic hangover characterized by three main pillars:

- The Banking Crisis: Financial institutions were suddenly left holding trillions of yen in unrecoverable loans backed by collateral (land) that was believed to never depreciate but now worth a fraction of its original appraisal.

- Deflation: As wealth evaporated, consumer spending collapsed. A psychological shift occurred where consumers delayed purchases, expecting prices to drop further tomorrow, which inherently choked off corporate profits.

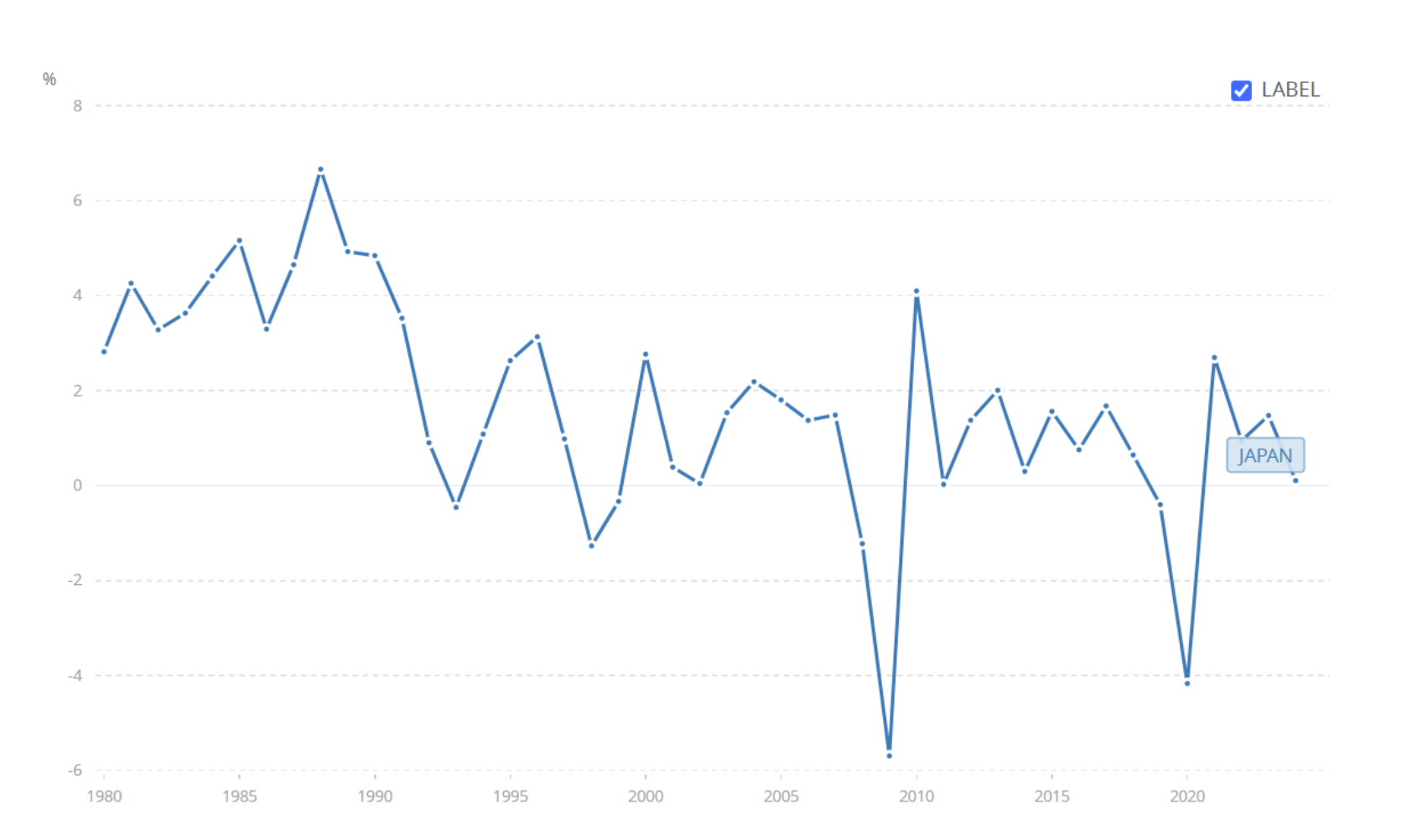

- Slow Economic Growth: Gross Domestic Product (GDP) growth flatlined, remaining near 0-1% for a generation as corporations and households focused entirely on paying down old debts rather than investing in foreign or domestic growth.

GDP Growth Rate Historical

Recovery Timeline

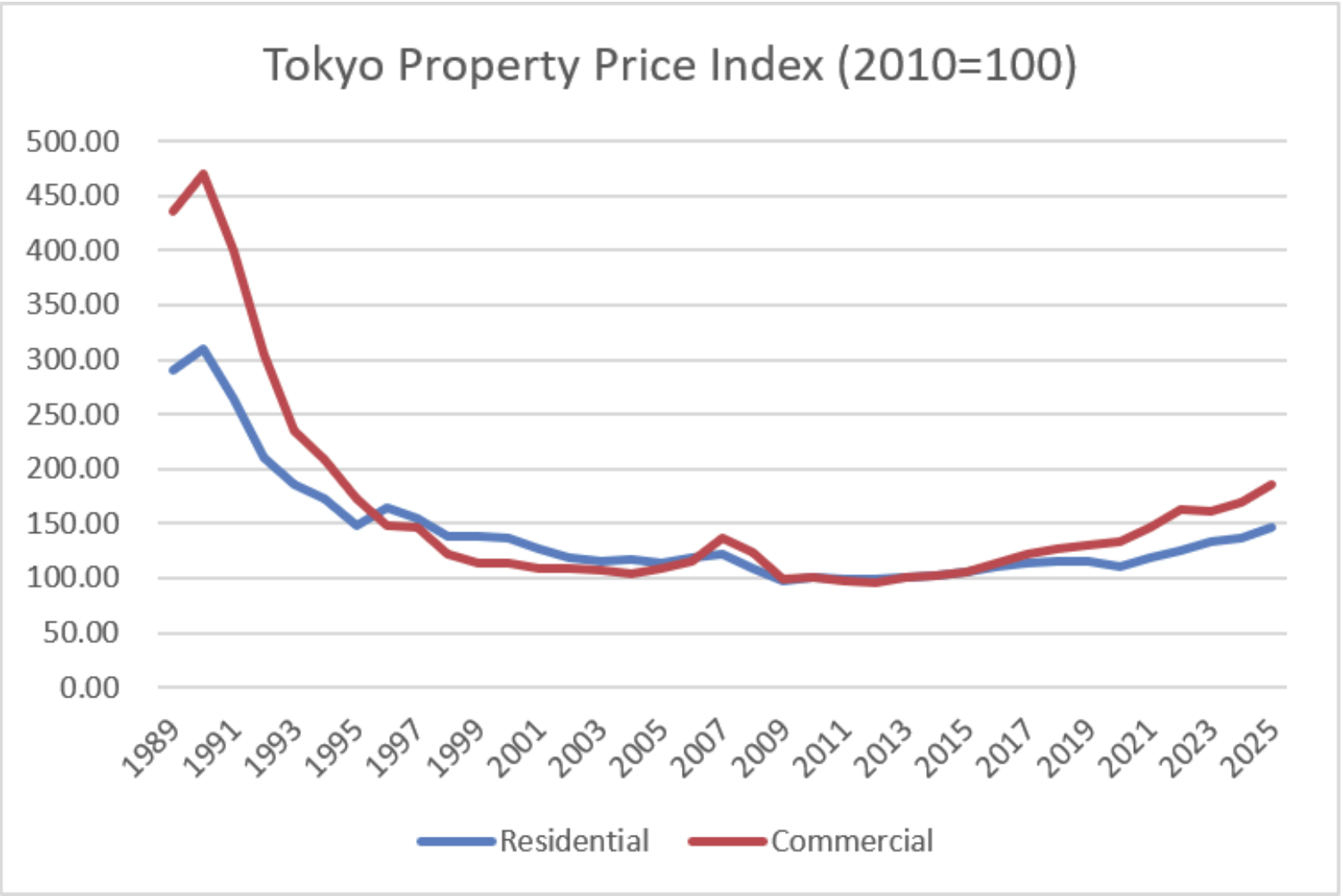

Commercial land prices in premier urban areas dropped by as much as 70% to 80% from their peak valuations.

It took nearly two decades for land prices in metropolitan Tokyo to firmly establish a bottom and begin a meaningful, structurally sound recovery.

For more details about the Japan real estate price history, especially after the 1990 bubble, also read:

🔗 Japan Property Price History: How Tokyo Property Prices Have Surpassed the 1990 Bubble Peak

5. Is Japan in a Real Estate Bubble Today?

With real estate prices in modern Tokyo recently matching or exceeding their 1989 nominal highs, many onlookers are asking if history is repeating itself.

However, an analysis of the structural fundamentals reveals that today's market is built on a vastly different foundation.

Why Today's Market Is Different

- Stricter Banking Regulations: Modern banks operate under stringent global capital requirements (such as Basel III guidelines). Loan-to-value ratios are tightly managed, preventing the flagrant over-collateralization seen in the 1980s.

- Conservative Lending: Credit is extended based on verifiable corporate cash flows or individual borrower income, rather than the blind assumption that "land prices only go up."

- Demographics and Speculation: Japan faces a shrinking, aging population, keeping nationwide demand balanced. Modern speculation is calculated and localized, driven by yield rather than frantic flipping.

Areas Experiencing Strong Growth

The current price appreciation is highly concentrated rather than nationwide. Demand is focused on:

- Central Tokyo: Luxury high-rise condominiums (tower mansions) in wards like Minato, Chiyoda, and Chuo.

- Foreign Investor Demand: International buyers utilize a historically weak yen to acquire premium, stable yields in a safe global city.

- Redevelopment Districts: Urban sub-centers explicitly targeted for modern infrastructure, commercial hubs, and transit upgrades.

6. Could Another Japan Property Bubble Happen?

While a systemic, country-wide replication of the 1990 crash is highly unlikely, a balanced look at the future market shows competing forces that investors must weigh.

Arguments For a Potential Bubble

- Prolonged Low Interest Rates: The Bank of Japan’s ultra-loose monetary stance over the past decade has created a cheap borrowing environment for home buyers.

- Concentrated Global Capital: Foreign institutional funds such as UBS see Tokyo as a safe-haven asset class, artificially decoupling prime urban real estate prices from local wage growth.

Arguments Against a Potential Bubble

- Demographic Realities: Outside of central urban cores, Japan has an oversupply of housing (including millions of akiya, or abandoned homes), which naturally caps systemic real estate inflation.

- Market Transparency: Real estate data, rental yields, and transaction historical metrics are incredibly transparent today, preventing the wild, uninformed speculative valuations of the 1980s.

🔗Also read🔗

Japan Real Estate Market Outlook 2026: Housing Investment Trends and Forecast

Tokyo Real Estate Outlook 2026: Market Trends and Investment Forecast

7. What Can Investors Learn from the 1990 Bubble?

The modern real estate landscape still offers massive opportunities, provided investors integrate the hard-learned lessons of the past:

- Price Momentum is Not a Guarantee: Never buy an asset solely because "prices rose last year." True value must be anchored to utility and intrinsic yield.

- Leverage is a Two-Edged Sword: Debt amplifies your gains in a rising market, but it accelerates your bankruptcy when liquidity dries up. Maintain conservative cash reserves.

- Cash Flow Over Speculation: A property should make financial sense on day one through reliable rental income. Speculating on future resale value is gambling, not investing.

- Location Metrics Move Independently: In a demographic decline, secondary and tertiary locations degrade quickly. High-quality, transit-connected urban locations remain resilient because they consolidate remaining population demand.

FAQ

1. How much did Japanese property prices fall after the 1990 bubble?

In major urban centers like Tokyo and Osaka, commercial land values crashed by up to 70% to 80% from their peak. On a nationwide scale, aggregate land values steadily declined for over 15 consecutive years before stabilizing.

2. Did the entire country experience the bubble?

Yes, though to varying degrees. While Tokyo, Osaka, and Nagoya experienced the most extreme, volatile asset spikes, the speculative mania trickled down to regional cities and resort areas, causing widespread overdevelopment across the country.

3. Are Tokyo property prices currently at bubble levels?

While nominal prices for new luxury condos in central Tokyo have bypassed 1989 peaks, current prices are supported by low interest rates, actual rental demand, and foreign capital. Unlike 1989, standard residential and regional land across Japan remains reasonably valued.

4. Why is foreign investment increasing in Japan today?

Foreign investors are drawn by the historically weak yen, which offers an immediate discount on purchase prices. Additionally, Japan offers strong property rights, political stability, and attractive borrowing spreads compared to other global metropolitan hubs.

🔗Also read🔗

Buying Property in Japan: Does a Weak Yen Benefit Foreign Investors?

5. Is buying Japanese property a good long-term investment?

It can be an excellent source of stable cash flow and wealth preservation if you focus strictly on high-demand urban areas (like central Tokyo or major redeveloped transit zones). However, properties in rural or declining demographic zones generally present high vacancy risks and depreciating asset values.

🔗Also read🔗

Japan Property Investment Guide for Foreigners

Summary

The Japan real estate bubble in 1990 serves as a powerful reminder that property prices do not rise forever. During the late 1980s, a combination of low interest rates, easy lending, and growing speculation pushed land values to unprecedented levels.

When the bubble finally burst, it left a lasting impact on Japan's economy and changed the way people viewed real estate investment for decades.

Today, Japan's property market looks very different from the one that existed during the bubble era. While prices in some parts of Tokyo have reached record highs, the market is supported by stronger regulations, more disciplined lending practices, and greater transparency.

Demand is also more concentrated in specific urban areas rather than spreading across the entire country.

That said, the lessons of the 1990 bubble remain just as relevant today. Investors should focus on long-term fundamentals such as location, rental demand, and sustainable cash flow rather than relying on rapid price appreciation.

By understanding what happened during Japan's bubble economy and why it collapsed, investors can better evaluate opportunities in today's market and make more informed decisions for the future.

Our team of seasoned professionals at PropertyAccess is dedicated to helping you navigate Japan’s real estate market with confidence.

With deep local knowledge and a commitment to personalized service, our experts are here to guide you every step of the way.