Japan Real Estate Market Outlook 2026: Housing Investment Trends and Forecast

Last Updated: May 14, 2026

Explore Japan’s 2026 real estate outlook, including market trends, price forecasts, risks, and investment opportunities in Japan’s dynamic property market.

Table of Contents

Supervised By: Hiroki Kazato

Japan has been a prime destination for global investment due to its economic stability and resilience, as well as its consistent urban redevelopment. For 2026, it is projected that the Japanese real estate market will remain a major destination, characterized by deepening polarization between its major metropolitan areas and peripheral regions.

In this article, we will explore the shifts in the market, highlighting the following major points:

- Macroeconomic Backdrop 2026

- Risk and Scenario Analysis

- Key Market Trends and Projections

- Market Drivers and Other Probabilities

- Investment Opportunities and Sectoral Outlook

- Insights from Our Experts

Also read 🔗 Tokyo Real Estate Outlook 2026: Market Trends and Investment Forecast 🔗 to learn more about market trends and opportunities specifically for Tokyo.

Macroeconomic Backdrop 2026

Interest Rate and Monetary Policy Outlook

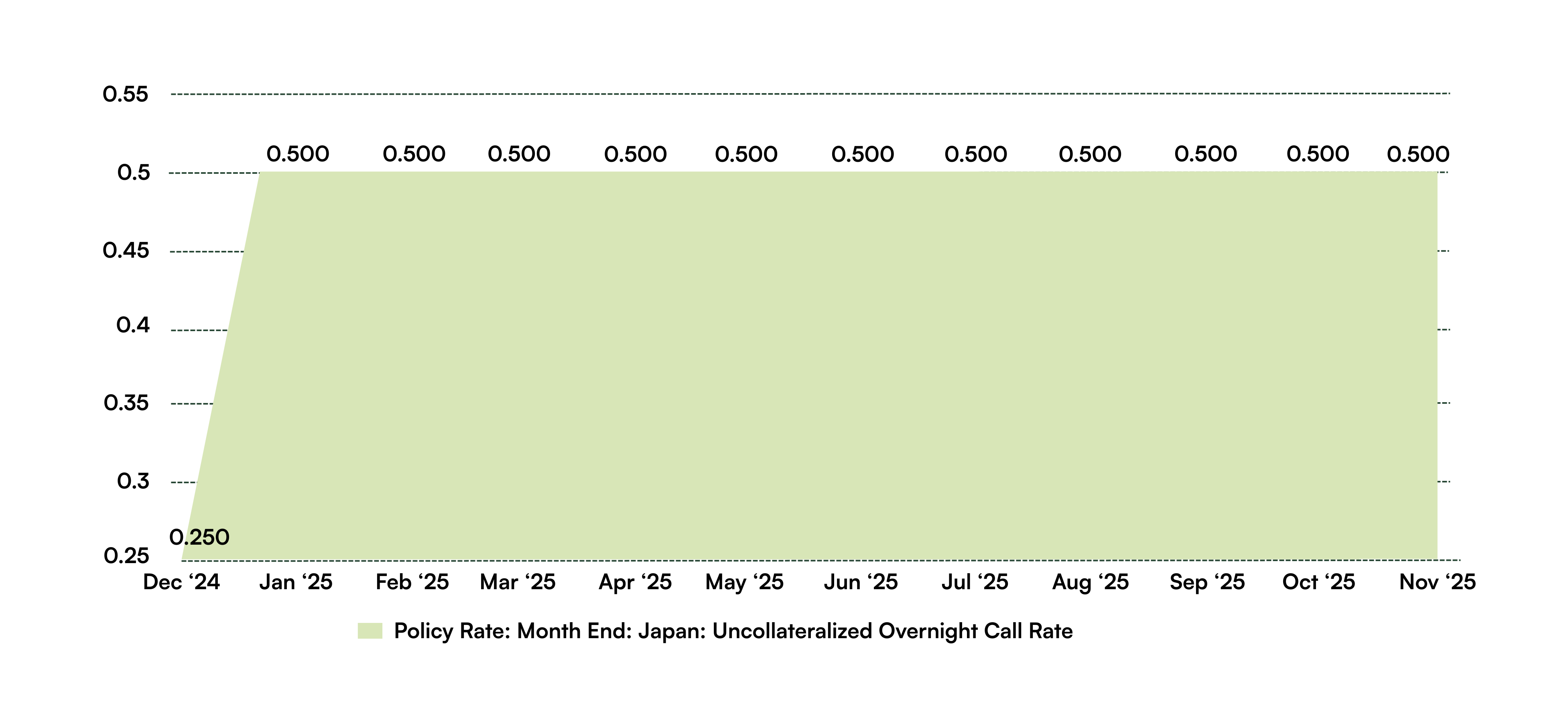

The expected interest hike in October 2025 was receded with the appointment of new Prime Minister Takaichi, shifting the interest hike to happen in early 2026 instead. The decision for the initial interest hike was based on persistently high inflation and a decline in the momentum of wage increases.

As of early December 2025, the Bank of Japan’s short-term policy interest rate is at 0.50%. However, the BoJ is signaling a strong chance to increase the rate to 0.75% at its next policy meeting in the same month. Through 2026, the BoJ is broadly expected to maintain its policy rate, approximately 0% to 1%. In the longer term, however, the BoJ has noted that its estimated neutral interest rate would be within the wide range of 1% to 2.5%. In the case that the BoJ raises interest rates more aggressively, borrowing costs would increase, softening real estate transaction volumes and compressing cap rates.

Japan’s Policy Rate from Mar 2006 to Nov. 2025 | Data Source: CEIC Data

Currently, the BoJ maintains monetary easing in order to achieve Japan’s inflation target of 2%. Based on an interview with Financial Times, BoJ Governor Kazuo Ueda predicts that underlying inflation will continue to rise towards the bank’s target. The adjustment of the degree of monetary easing would help to ensure that the financial and capital markets remain stable, placing Japan’s economy on a sustainable growth trajectory during a period of upward pressure on wages and prices, while interest rates remain extremely low. This environment would be beneficial for real estate investment and financing conditions.

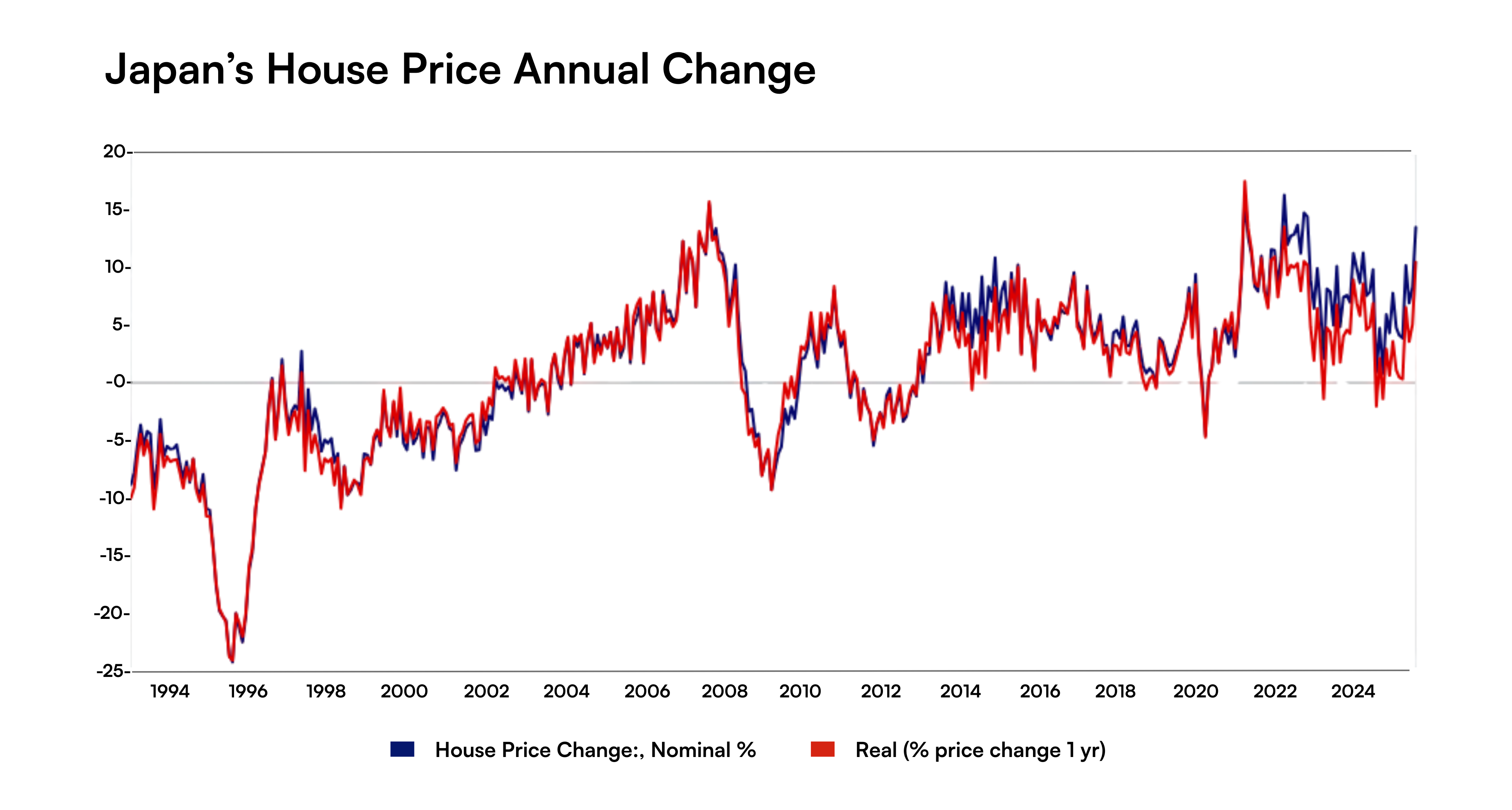

Relationship Between Inflation Rate and Rent Growth

Have Rents Kept Pace with Price Increases?

Rent in Japan is slowly catching up to broader inflation in major metropolitan areas like Tokyo, Osaka, and Fukuoka due to urban migration, constrained supply, and rising maintenance costs. However, for other regional areas, rents have only risen at modest rates, typically below the Consumer Price Index. This resulted in slightly negative (inflation-adjusted) rent growth.

Overall, Japan continues to face low growth coupled with population decline, yet the largest urban areas, namely Tokyo, Osaka, and Fukuoka, display sustained population inflows and a relatively stronger economic performance, which reinforces their long-term resilience ideal for real estate investment.

Risk and Scenario Analysis 2026 (Base/ Upside/ Downside)

Risk is present in any investment. It is just a matter of what risk level is acceptable to make your investment worthwhile. We will evaluate three practical scenarios: baseline, upside, and downside, based on key risks: (1) interest rate hikes, (2) foreign exchange volatility, (3) strengthened regulations, and (4) natural disaster risks.

1. Baseline Scenario: Gradual Normalization and Stable Market Conditions

In the assumption that:

(1) BoJ continues to deploy gradual interest rate adjustments,

(2) the Japanese yen stays within moderate and stable trading range,

(3) no major regulatory shifts on foreign ownership, and

(4) natural disasters remain within historical norms

Real estate activity will remain stable. Financing will be relatively affordable with stable cap rates. There will be a positive leasing momentum in urban markets due to continued population inflow. Moderate rent growth will be expected in supply-constrained markets. And international investments will remain steady.

2. Upside Scenario: Yen Depreciation Trend and Investor-Friendly Environment

In the case that:

(1) the Japanese yen further depreciates attracting more tourism,

(2) visitors surpass projections boosting hospitality, retail, and logistics sectors,

(3) restrictions on short-term rentals are eased and other regulations become more flexible, and

(4) no major natural disasters occur

A strong competitive real estate market will be present. In major cities, increased foreign capital inflows may lead to cap rate compression. This will allow current property sellers and owners to experience boosted asset value while buyers will experience higher prices for less initial yield. The hospitality sector may outperform with improved average daily rates because of high tourist demand. Retail properties in strategic locations may experience strong rent growth. And investor transaction activity will increase due to the expected continuous inbound growth.

3. Downside Scenario: Sharp Interest Hikes, Forex Reversal, and Regulatory Restrictions

In the case that:

(1) interest rates are suddenly hiked up due to persistent inflation or yen instability,

(2) sharp yen appreciation which will reduce tourism and foreign demand,

(3) restrictions are introduced to foreign ownership with additional real estate taxes, and

(4) a major natural disaster that disrupts economic activity occurs

Inbound real estate activity will contract. Transactions will slow down due to higher borrowing costs. Cap rates will widen, especially for secondary locations. There will be less foreign investor participation which will reduce property liquidity. Operational costs will rise in order to mitigate natural disaster risks. And hospitality and retail segments will experience softening leasing demand.

Key Market Trends and Projections

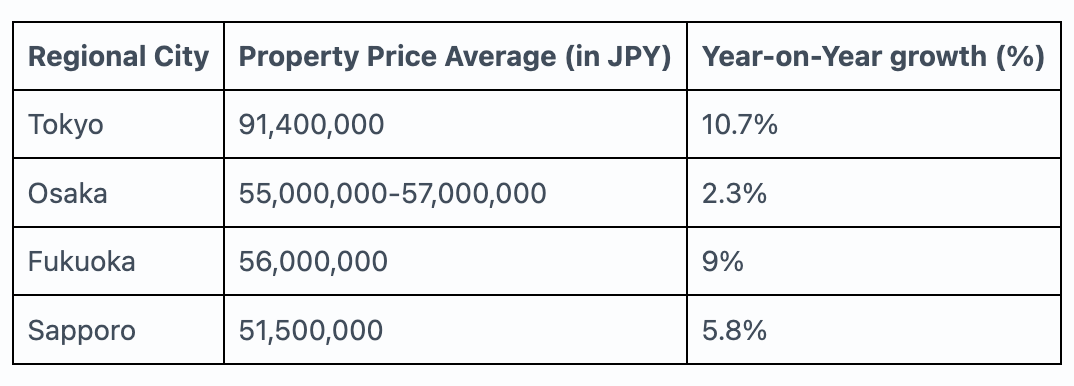

Japan has experienced strong national and urban growth in property prices in 2025, with Tokyo leading the luxury segment. The average residential price in Tokyo is 91.4 million JPY, a 10.7% increase year-on-year. It is forecasted that prices will continue to increase in major cities by 5-6% in 2026. Supply constraints will fuel this growth as demand outweighs the current property reserves.

While Tokyo commands the highest premiums in the country, other regional cities offer different value propositions with a more affordable price range. On the other hand, rural areas present significantly different pricing, typically ranging from 20 to 25 million JPY. Urban migration patterns have continued to support this decline and will continue to do so as the younger generation settles in urban areas.

Data Source: Bambooroutes

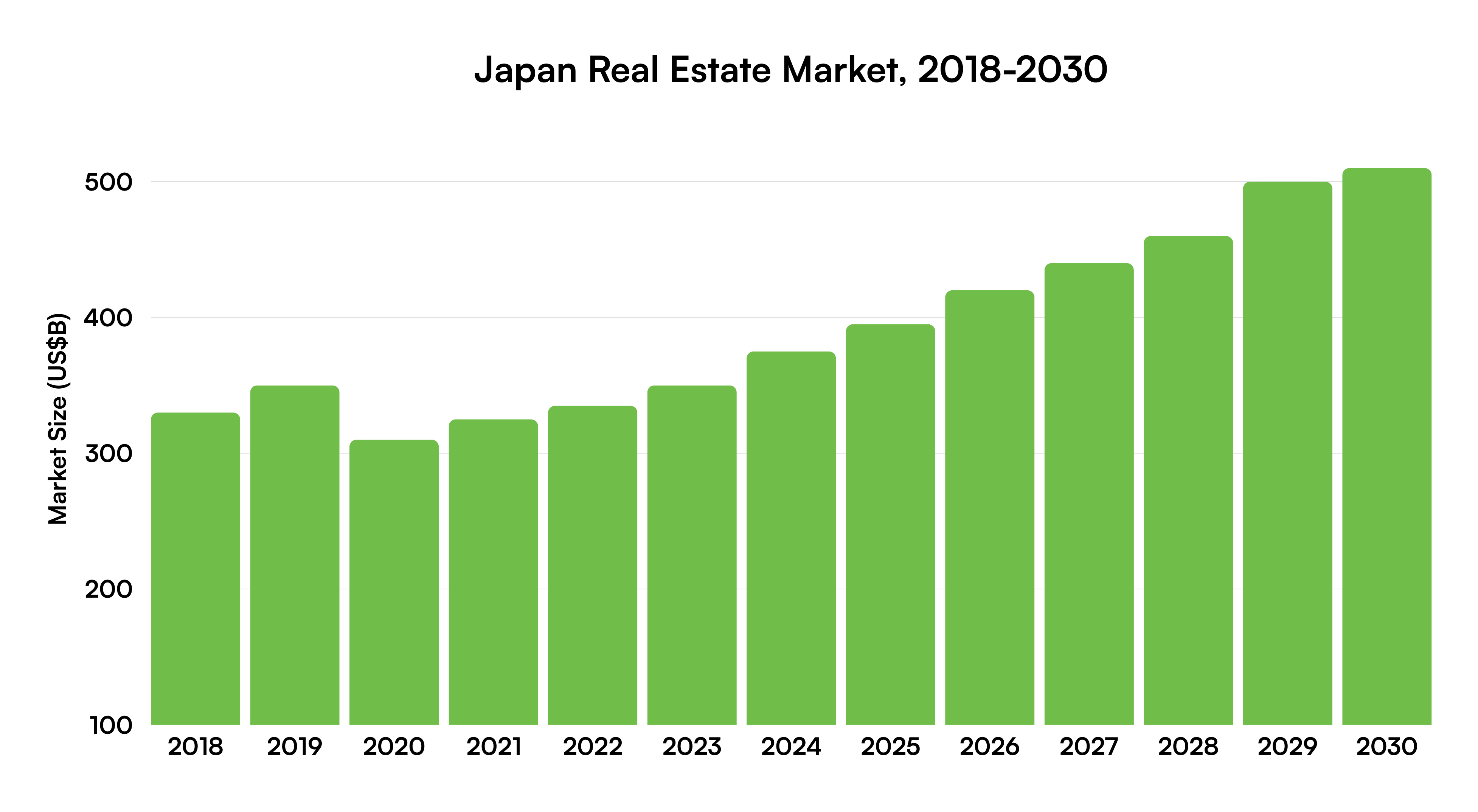

Residential continues to be the largest revenue-generating property type. By 2030, Japan’s real estate market is forecasted to reach a total revenue of over 533 billion USD, with the residential sector leading. Based on historical data from 2018 to 2023, the expected compound annual growth rate is projected to be 6.6% from 2025 to 2030.

Data Source: Grand View Research

Condominiums continue to be the key driver in the residential sector growth. According to the JREI Existing Condominium Price Index by Japan Real Estate Institute, there has been a 10.47% year-on-year increase in condominium prices in the Tokyo metropolitan area as of July 2025. Furthermore, Tokyo has the steepest rise in price by 12.62% followed by Chiba at 7.55%, Kanagawa at 6.58%, and Saitama at 4.63%. For newly built condominiums alone, Tokyo’s prices surged more than 20% year-on-year in July 2025, according to the Land Research Institute.

Note: Japan (Tokyo) House Price Index: Average Price of Existing Condominium Sales

Data Source: The Land Institute of Japan

National land prices mark the strongest growth in 34 years. Land prices rose by 2.7% in 2025, following the price increase of properties due to urban concentration, international capital flows, and limited supply in prime locations. This upward momentum is projected to continue, potentially creating a wealth effect for existing property owners.

Most real estate transactions are foreign investments. In 2025, over 27% of property purchases in Japan were made by international investors. This represents a great increase from the 21% of 5 years ago, mostly due to the weak yen and Japan’s straightforward legal structure. In Tokyo alone, 20 to 40% of the new apartments were sold to foreigners, according to Mitsubishi UFJ Trust & Banking Corp. As there are currently no stringent regulations on foreign real estate ownership, it is anticipated that there will be a surge in foreign investment to take advantage of this favorable environment.

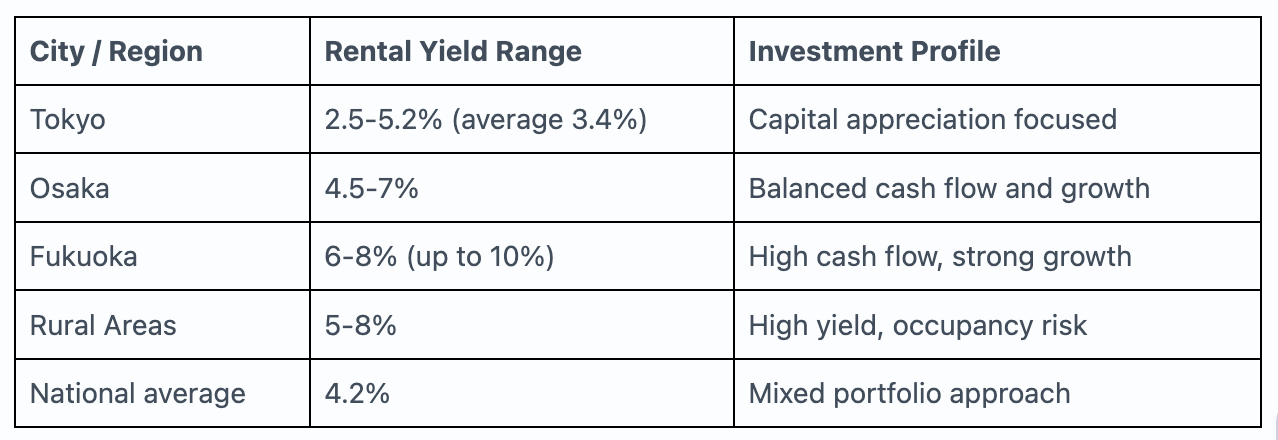

Regional cities offer strong cash flow. More real estate hotspots are emerging in Japan as these regional cities provide robust rental yields. Overall, the national average is 4.2% with Osaka and Fukuoka presenting compelling yields compared to Central Tokyo.

Data Source: Bambooroutes

Market Drivers and Other Probabilities

Japan’s 2026 real estate outlook is heavily influenced by the polarization of urban and rural regions. These persistent factors continue to shape the market, creating both opportunities and risks for investors in the property segment.

1. Rising land prices. There has been an upward trend in the prices of land since late 2025, continuing into 2026. This is driven by the urban concentration of the population, alongside increasing foreign investment amid supply constraints, especially for prime locations such as Tokyo.

2. Fluctuating currency. The yen’s exchange rate has been affecting the foreign investor activity. The Japanese currency has been fluctuating throughout 2025, predominantly being on the weaker side. International buyers are capitalizing on the currency discount to purchase luxury residential properties.

As of November 24, 2025, Takuji Aida, adviser to Prime Minister Sanae Takaichi, stated that Tokyo can actively intervene in the currency market in order to offset the negative effects of the weak yen on the country’s economy. Investors are advised to remain vigilant in case of government intervention to slow down or prevent the yen from weakening further.

3. Widening price gap between Tokyo and regional cities. Due to the demographic pressure brought about by urban migration, price gaps have broadened between major metropolitan areas and peripheral regions. For reference, the average rural property price ranges from 20 to 25 million JPY, while the average price in Tokyo is 91.4 million JPY.

Foreign demand in major urban areas, such as Tokyo, hikes up the property prices, giving fierce competition to domestic buyers.

4. Demographic shift in leasing preferences. There is a growing interest in sustainable and environmentally friendly buildings. More tenants are seeking buildings that are energy efficient. The aging population is driving preferences and demand for housing near healthcare facilities, which are built to be senior-friendly.

5. Demographic decline in rural areas. Rural areas continue to face rising vacancy rates and minimal construction due to the consistent urban migration. The countryside is experiencing an oversupply in properties, with a number of them turning into “akiya homes” or abandoned homes.

The Japanese government has been incentivizing the reuse and renovation of such akiyas to mitigate the rising number of abandoned homes in rural Japan. As of 2023, approximately 13% of the country’s residential properties were abandoned, totaling roughly 9 million homes. This number may continue to rise if this trend continues.

6. Tax incentives stimulate property investment. The Japanese government has raised the tax-free income threshold from 1.03 million JPY to 1.6 million JPY in 2025. Other property tax incentives were also given for vacant home renovations, such as solar installation subsidies, relaxed floor area ratios, and stamp duty reductions. As of late 2025, there are still no restrictions on foreign property ownership. However, this might change in 2026 as the government may consider tightening regulations.

Investment Opportunities and Sectoral Outlook

In the constantly changing global economic and political landscape, Japan’s real estate market remains compelling, especially for foreign investors. Strategic investment in prime assets and high-growth sectors has proven to provide defensive returns and can become a hedge against global unpredictability.

Each sector in the real estate industry varies significantly in terms of performance, with some being stronger than others in 2025. These may serve as opportunities or reference points for your investment decisions coming into 2026.

Residential Property Sector

The residential sector has been consistent for the past years in being the strongest performing in the Japanese market. Core metropolitan areas such as Tokyo and Osaka provide robust leasing growth due to rising prices, pushing local residents to the rental market to satisfy demand.

Regional growth hubs for residential are emerging, such as Fukuoka and Sapporo, with these areas experiencing rising demand due to favorable demographic shifts and lower entry costs compared to major city areas. Rental yields are showing promising growth and can present opportunities for investors looking beyond Tokyo.

Rural and other peripheral areas are struggling with urban migration, making the liquidity low for properties in these areas. Investment risk may be high in the case of pursuing capital growth and rental yield.

Commercial Property Sector

The traditional commercial sector’s market offers stability, while the more specialized segments provide more noticeable growth. Office demand in prime Tokyo is experiencing a gradual rebound as hybrid and in-person work arrangements become more prevalent. This stabilizes the office rentals, improving vacancy rates.

Hospitality and retail properties are undergoing significant growth as international visitor numbers reach record-breaking highs while being aided by the weak Japanese yen. The operational performance of hotel properties remains strong, making them a good target for high-income-generating opportunities. Furthermore, prime retail assets within luxury districts, namely Ginza and Omotesando, are performing remarkably well because of high-spending tourists.

Logistics and Industrial Property Sector

The sustained growth of e-commerce mainly supports the logistics sector. Although the new supply in 2025 created some vacancies, it is anticipated to decline greatly from 2026 as construction costs and labor shortages increase. This supply bottleneck is expected to make a strong rental growth potential for existing facilities in major city areas.

With the ongoing rise in demand for AI and cloud services, data centers in major hubs (Kanto and Kansai regions) are expected to deliver a robust performance in 2026 for the industrial sector. Significant capital inflows are expected to be dedicated to new developments and infrastructure build-outs to accommodate the massive demand.

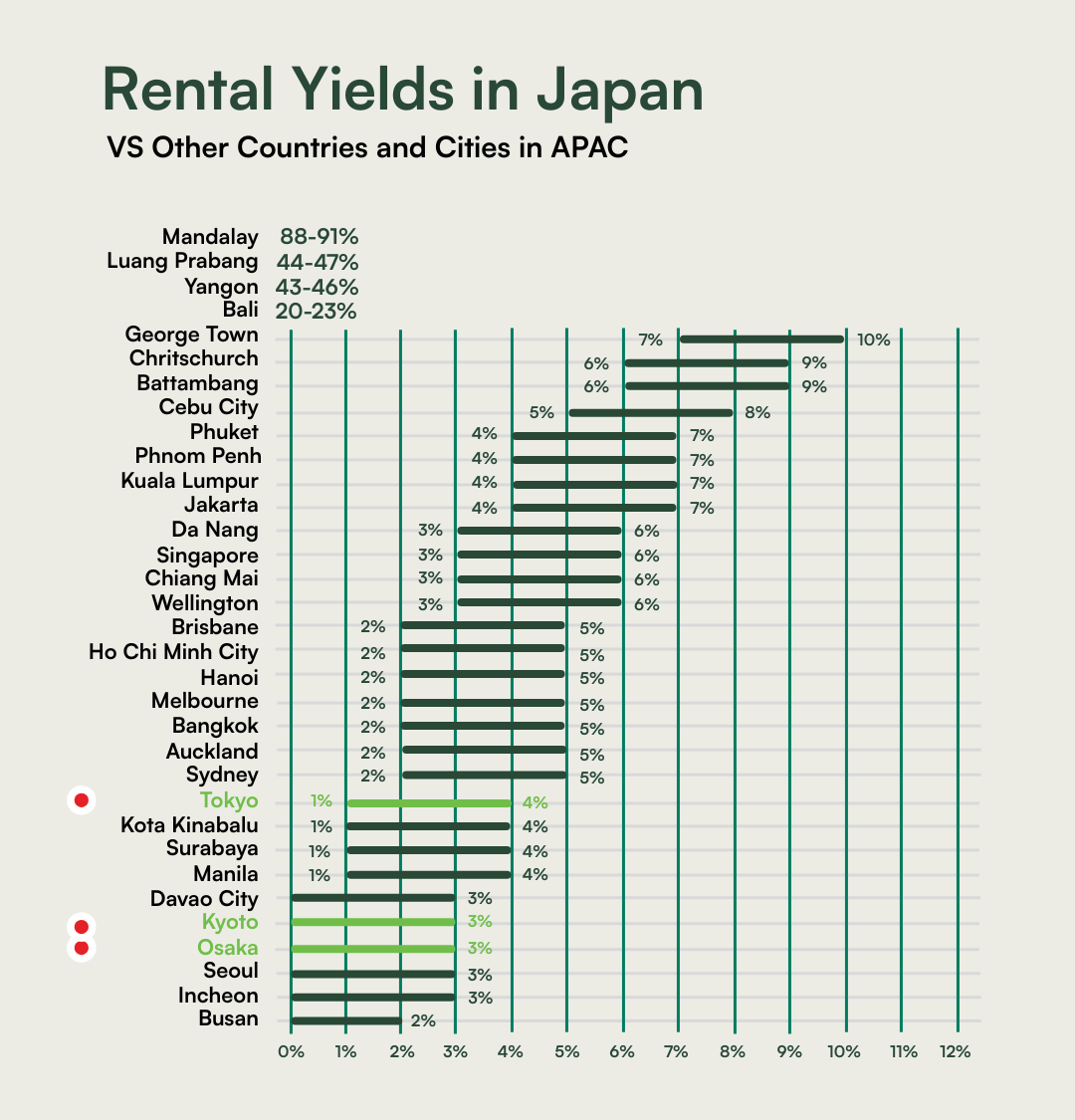

Below is a quick comparison of rental yields encompassing the sectors of major cities in Japan versus neighbouring countries.

Data Source: Ministry of Land, Infrastructure, Transport and Tourism, Japan, Numbeo, IMF, World Bank, Bambooroutes

Insights from Our Experts

Japan is expected to continue experiencing moderate growth in 2026 with increasing urban and rural divergence. Residential prices are projected to rise, with Tokyo leading the price growth with 5 to 6%.

Attractive markets you may want to consider for 2026 include Tokyo, Osaka, Kyoto, and Fukuoka. With the growing prevalence of hybrid and in-person work models, these major hubs spark demand primarily in the rental market.

Our experts have shared their insightful perspectives on the Japanese real estate outlook for 2026. Here are some of their noteworthy statements:

Hiroki Kazato, CEO and Founder of PropertyAccess

“Residential properties remain to show the strongest performance in the real estate industry. This direction is expected to be the trend in 2026, especially for properties located in the five central wards and along the major subway lines such as the Yamanote Line. Limited supply of new condominium units, as well as rising construction and material costs are pushing property prices higher for both primary and secondary (used) property markets.

As the government considers new and stricter regulations on foreign real estate ownership, it is expected that a wave of last-minute purchases by foreign individuals and corporations will occur. This trend will further drive prices up, especially in Tokyo’s main wards. Overall, Japan stands as one of the most competitively priced and resilient investment markets globally heading into 2026.”

Miel Soriano, Business Development Lead and Asset Manager

“Japan’s residential and multifamily sectors are set for a promising outlook heading into 2026. Compared with other high-end global markets, Japanese real estate remains attractively priced, drawing sustained interest from both domestic and international investors—especially with the yen still weak and financing conditions relatively supportive. Strong rental demand in urban hubs continues to drive stable occupancy and yields, while booming tourism is fueling growth in Airbnb and other short-stay formats, particularly in cities like Tokyo, Osaka, Sapporo, and Fukuoka where regulated short-term operations are gaining traction.

At the same time, elevated prices in new developments are likely to increase liquidity and competitiveness in the secondary market, where well-located existing assets present compelling opportunities. While investors should remain mindful of potential rate shifts, regulatory adjustments, and construction-cost pressures, these same dynamics create openings to reposition older multifamily properties, add short-stay components where legally viable, and expand portfolios in high-growth submarkets.”

Our team of seasoned professionals at Property Access is dedicated to helping you navigate Japan’s real estate market with confidence.

With deep local knowledge and a commitment to personalized service, our experts are here to guide you every step of the way.